Introduction

TL;DR Insurance claims processing carries a weight that most industries never experience. Every claim represents a person in a difficult moment. A flooded home. A totaled car. A medical emergency. That person needs resolution fast. The industry, historically, has delivered the opposite. Slow reviews. Manual data entry. Weeks of back-and-forth. The operational cost of this slowness is enormous. The human cost is just as real. Something has to change. Automating insurance claims processing using OCR and LLMs is now that change. Optical Character Recognition reads documents at machine speed. Large Language Models understand their content at human depth. Together, they compress claim cycle times from weeks to hours. This blog breaks down exactly how this technology works, where it creates real value, and what insurers need to know before building or buying these systems.

Table of Contents

The State of Claims Processing Today

Claims processing has not changed structurally in decades. A claim arrives. A human reads it. That human enters data into a system. Another human reviews the data. Someone checks policy coverage. Someone else requests more documents. A supervisor approves or denies. The claimant waits throughout this chain.

The Scale of the Problem

The U.S. insurance industry processes over one billion claims annually. Health insurance alone accounts for more than 900 million claims per year. Property and casualty claims add hundreds of millions more. Each one requires document intake, data extraction, coverage verification, fraud screening, and payment authorization. At this volume, even small inefficiencies multiply into massive operational burdens.

Average claim cycle time in property insurance runs 30 to 45 days. Health insurance claims average 14 to 30 days for complex cases. Auto claims that should resolve in a week drag to three or four weeks when adjusters face backlogs. These delays cost insurers money in operational overhead and cost claimants time they cannot afford.

Why Manual Processing Fails at Scale

Manual processing fails for predictable reasons. Human data entry creates errors. Studies show manual data entry error rates between 1% and 4%. At one billion claims, even a 1% error rate means ten million incorrect records annually. Each error requires correction, which costs more than processing the original claim correctly.

Document variety compounds the problem. Claims arrive as PDFs, photos, handwritten notes, fax copies, and scanned forms. Each format requires different handling. Adjusters context-switch constantly. Cognitive fatigue increases error rates. Volume grows every year. Hiring keeps pace for a while. Then it becomes economically unsustainable.

Automating insurance claims processing using OCR and LLMs addresses every one of these failure points directly. It reads any document format. It extracts data accurately. It scales without hiring. It never gets tired.

What OCR Does in the Claims Pipeline

Optical Character Recognition converts visual document content into machine-readable text. In claims processing, this is the first essential step. Documents arrive in formats that downstream systems cannot read natively. OCR bridges that gap.

Traditional OCR Versus Modern OCR

Traditional OCR engines like Tesseract work well on clean, typed documents with standard layouts. Insurance claims are rarely clean. They include handwritten notes in margins. They include mixed fonts. They include tables with irregular structure. They include stamps, watermarks, and poor scan quality. Traditional OCR fails on these inputs at rates that make automation impractical.

Modern OCR systems use deep learning to handle these challenges. They recognize handwriting with accuracy rates above 90% on typical insurance documents. They extract structured data from tables without requiring predefined templates. They handle rotated pages, low-resolution scans, and mixed document types. Modern OCR is not just text recognition. It is intelligent document understanding.

Key Document Types in Claims Processing

Claims processing involves many document types. Each poses its own OCR challenges. Medical records contain dense clinical terminology mixed with handwritten annotations. Repair estimates use structured tables with part numbers and cost breakdowns. Police reports mix typed fields with free-text narrative sections. Explanation of Benefits forms have complex nested structures. Death certificates follow state-specific formats that vary across jurisdictions.

Strong OCR systems in the context of automating insurance claims processing using OCR and LLMs handle all of these formats without manual configuration per document type. They classify the document type automatically. They apply the appropriate extraction logic. They flag low-confidence extractions for human review rather than silently producing wrong output.

OCR Accuracy and Its Business Impact

OCR accuracy directly determines downstream processing quality. A 95% character accuracy rate sounds strong. On a 1,000-character document, it means 50 errors. A policy number with one wrong digit routes the claim incorrectly. A dollar amount with a transposed digit creates a payment error. The target for production insurance OCR systems is 99%+ on typed text and 92%+ on handwritten content, with human review triggered automatically below those thresholds.

What LLMs Add to Claims Processing

OCR extracts text. LLMs understand it. This distinction defines why automating insurance claims processing using OCR and LLMs works in ways that OCR alone never could.

Understanding Context and Intent

Insurance documents contain information that requires interpretation, not just extraction. A medical record might say “MVA with cervical strain” — which an LLM correctly interprets as a motor vehicle accident with a neck injury. A repair estimate might list “OEM fascia assembly” — which an LLM understands as an original equipment manufacturer front bumper. These interpretations require domain knowledge and language understanding that OCR and rule-based systems lack entirely.

LLMs bring this understanding to the claims workflow. They read extracted text and derive meaning from it. They identify relevant facts. They connect information across multiple documents in the same claim. A claim for water damage involves a plumber’s invoice, a contractor estimate, a property inspection report, and a homeowner statement. An LLM reads all four documents and builds a coherent picture of the damage event, its cause, and its scope.

Coverage Determination Assistance

Coverage determination requires comparing claim facts against policy language. Policy documents are notoriously complex. They contain exclusions within exclusions. They use defined terms that carry specific legal meanings. They reference schedules and endorsements. Human adjusters spend years learning to navigate this complexity correctly.

LLMs trained on insurance policy language can compare claim facts against policy terms accurately. They identify applicable coverage clauses. They flag potential exclusions. They highlight ambiguities that require human review. This LLM-assisted coverage analysis is one of the highest-value applications of automating insurance claims processing using OCR and LLMs. It accelerates adjudication without removing human judgment on complex or contested cases.

Narrative Generation and Communication

Claims processing generates substantial documentation. Adjuster notes. Coverage determination letters. Request for additional information letters. Denial letters with regulatory-compliant language. Each document takes time to write correctly. Errors in these communications create compliance risk and policyholder dissatisfaction.

LLMs draft these documents from structured claim data. A denial letter with proper legal language, specific exclusion citations, and appeal instructions generates in seconds. A coverage explanation letter that a policyholder can actually understand generates with the same effort. The adjuster reviews and approves. The quality is consistent. The speed is transformative.

Fraud Signal Detection

Fraud costs the U.S. insurance industry an estimated $308 billion annually. LLMs contribute to fraud detection by analyzing claim narratives for inconsistency patterns. They compare claimant statements across documents for internal contradictions. They flag unusual terminology that appears in known fraud patterns. They identify timing anomalies, such as policies taken out days before a claim. Combined with traditional fraud scoring models, LLM-based narrative analysis improves fraud detection rates meaningfully without increasing false positive rates.

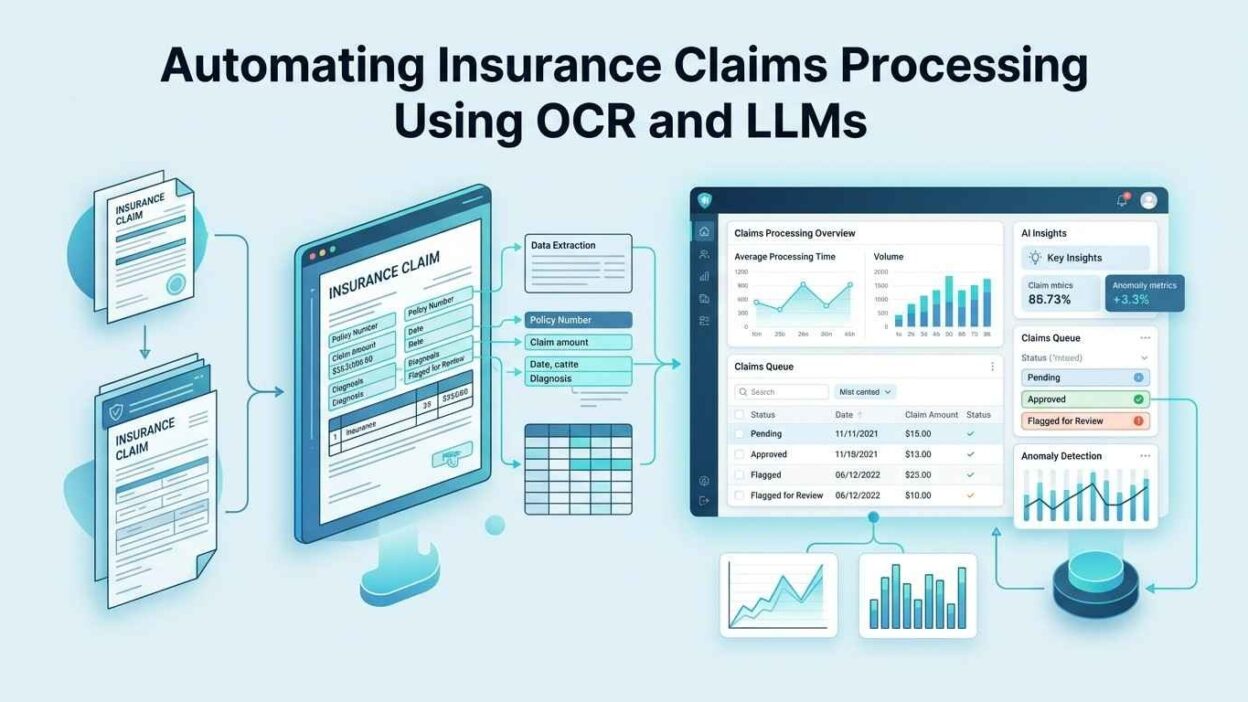

The End-to-End Architecture of an Automated Claims System

Understanding how the full system works helps leaders and architects evaluate what they are building or buying. Automating insurance claims processing using OCR and LLMs is not a single tool. It is a pipeline of coordinated components.

Document Ingestion Layer

Claims arrive through multiple channels. Email attachments. Web portal uploads. Mobile app photos. Fax-to-digital conversions. Mail scanning services. The ingestion layer receives documents from all of these channels. It normalizes them into a standard internal format. It assigns each document to its claim record. It triggers the OCR pipeline for processing.

The ingestion layer must handle high volume without dropping documents. It must maintain chain of custody for regulatory compliance. It must store original documents alongside processed versions. These are infrastructure requirements, not AI requirements. They must be solid before AI layers deliver value.

OCR and Document Classification Layer

Ingested documents enter the OCR pipeline. The system classifies each document by type. It applies appropriate extraction logic. It produces structured data with confidence scores for each extracted field. Low-confidence fields trigger a human review queue rather than proceeding automatically. High-confidence extractions flow directly to the next stage.

This layer is the foundation of automating insurance claims processing using OCR and LLMs. Its accuracy determines the quality of everything downstream. Teams that underinvest here discover their problems at the payment stage, which is far more expensive to fix.

LLM Analysis and Reasoning Layer

Structured data from the OCR layer feeds into the LLM layer. The LLM receives all documents for a claim simultaneously. It analyzes the claim facts, compares them against policy terms, identifies coverage implications, flags fraud signals, and generates a structured analysis report. This report becomes the adjuster’s primary working document.

The LLM layer also handles communication drafting. It generates status update messages, information request letters, and determination communications. All LLM outputs carry confidence scores and reasoning traces. Adjusters see the LLM’s reasoning, not just its conclusions. This transparency builds trust and enables effective human oversight.

Human Review and Decision Layer

Full automation suits only the simplest, lowest-risk claims. Most claims benefit from human review of LLM-generated analysis. The workflow routes claims by complexity score. Straightforward claims with high-confidence extractions and clear coverage go straight to payment authorization after a quick adjuster review. Complex claims, high-value claims, and flagged fraud cases receive full adjuster attention. The LLM handles preparation. The adjuster handles judgment.

Payment and Closure Layer

Approved claims route to payment authorization. The system generates payment records, triggers disbursement, and updates claim status. It sends policyholder notifications. It archives all documents and decision records for regulatory compliance. Complete audit trails document every automated step and every human decision throughout the process.

Real-World Results from Early Adopters

The business case for automating insurance claims processing using OCR and LLMs is not theoretical. Early adopters across health, property, auto, and life insurance lines report consistent patterns of improvement.

Cycle Time Reduction

Lemonade, an AI-native insurer, processes some claims in seconds. Their auto-adjudication model handles straightforward claims without human intervention. Cycle times that averaged weeks at traditional insurers drop to hours or minutes. Traditional insurers implementing similar systems report 40–60% reductions in average cycle time within the first year of deployment.

Cycle time reduction is not just an operational metric. It drives policyholder satisfaction directly. J.D. Power research consistently shows that claim resolution speed is the top driver of insurer satisfaction scores. Faster resolution translates directly into higher renewal rates.

Cost Per Claim Reduction

Labor represents 60–70% of claim processing costs at most insurers. Automation reduces the labor input per claim without reducing claim quality. Early adopters report cost-per-claim reductions of 30–50% on auto-adjudicated claim types. Simple health insurance claims that previously required 15 minutes of adjuster time process in under two minutes with LLM assistance. At scale, these savings compound dramatically.

Accuracy Improvement

Manual data entry error rates of 1–4% drop to under 0.5% with OCR-based extraction systems. LLM-assisted coverage analysis reduces coverage determination errors by 20–35% compared to manual review alone. Fewer errors mean fewer claim re-opens. They mean fewer regulatory complaints. They mean fewer legal disputes over incorrect denials.

Implementation Challenges and How to Address Them

Automating insurance claims processing using OCR and LLMs delivers strong results when implemented thoughtfully. Several challenges require deliberate planning.

Data Privacy and Regulatory Compliance

Insurance claims contain some of the most sensitive personal data that exists. Medical diagnoses. Financial records. Legal judgments. HIPAA in health insurance. GDPR in European markets. State-specific data handling regulations in property and casualty. Every component of the automation pipeline must handle this data with appropriate security controls.

Data residency requirements matter. Some regulations require claim data to remain within specific geographic boundaries. Cloud-based LLM APIs may not satisfy these requirements. Teams must evaluate on-premises LLM deployment options or certified cloud environments for regulated workloads.

Model Accuracy on Edge Cases

LLMs perform strongly on common claim types and standard document formats. Edge cases challenge them. An unusual policy endorsement. A claim involving a rare medical procedure. A document in an unexpected language or format. Production systems must detect edge cases and route them to human review rather than processing them with unwarranted confidence.

Build a continuous improvement loop. Track cases where LLM analysis was incorrect. Use those cases to improve prompts, fine-tune models, and update routing logic. Automating insurance claims processing using OCR and LLMs improves over time when teams invest in feedback loops.

Change Management and Adjuster Adoption

Adjusters have strong intuitions about claim quality. They resist automation that produces outputs they cannot understand or verify. LLM systems that show their reasoning earn adjuster trust. Systems that produce conclusions without explanation do not. Design the adjuster interface to surface LLM reasoning clearly. Show which documents supported which conclusions. Let adjusters override and correct LLM outputs easily. Log those corrections and use them to improve the system.

Selecting the Right OCR and LLM Stack

Choosing technology components for automating insurance claims processing using OCR and LLMs requires matching tool capability to insurance-specific requirements.

OCR Technology Options

AWS Textract handles structured forms and tables well. It integrates natively with AWS infrastructure. Google Document AI offers strong performance on complex documents with mixed content types. Azure Form Recognizer handles custom document templates with training-based configuration. For handwriting-heavy documents, Google Document AI currently leads on accuracy benchmarks. For structured insurance forms with standard layouts, Textract offers the simplest integration path.

LLM Options for Insurance Workflows

GPT-4o and Claude Sonnet offer the strongest reasoning performance on complex insurance documents. Both handle long documents with multiple interconnected sections well. For regulated environments requiring data residency control, Azure OpenAI Service and Anthropic’s dedicated cloud deployments offer compliance-ready options. Open-source models like Llama 3 70B and Mixtral offer strong performance for teams requiring fully on-premises deployment. Fine-tuning on insurance-specific data improves accuracy on domain terminology and policy interpretation tasks.

Integration with Core Insurance Systems

The automation pipeline must integrate with claims management systems. Guidewire, Duck Creek, and Majesco are the dominant platforms in property and casualty. HealthEdge and TriZetto lead in health insurance administration. API integrations with these systems allow the automation layer to read policy data, write claim decisions, and trigger payment workflows without manual data transfer.

Supporting Concepts

Intelligent Document Processing

Intelligent document processing combines OCR, classification, extraction, and validation into a unified workflow. It goes beyond simple text recognition to understand document structure and content semantics. IDP platforms form the foundation of automating insurance claims processing using OCR and LLMs at enterprise scale.

Straight-Through Processing

Straight-through processing describes claim workflows that complete from submission to payment without human intervention. Auto-adjudication rates of 30–60% are achievable on straightforward claim types with mature automation systems. Higher STP rates reduce cost per claim and accelerate policyholder resolution.

AI-Assisted Adjudication

AI-assisted adjudication uses LLM analysis to support human adjuster decisions rather than replace them. The LLM prepares the analysis. The adjuster makes the final call. This model suits complex and high-value claims where full automation carries unacceptable risk. It is the dominant deployment pattern for automating insurance claims processing using OCR and LLMs in its early enterprise adoption phase.

Natural Language Processing in Insurance

NLP capabilities within LLMs enable insurance-specific understanding. They parse clinical terminology in medical records. They interpret legal language in policy documents. They extract structured facts from unstructured adjuster notes. NLP bridges the gap between human-written documents and machine-processable data across the full claims workflow.

Frequently Asked Questions

How accurate is OCR on handwritten insurance documents?

Modern deep learning OCR systems achieve 90–95% character accuracy on clearly handwritten content. On poor-quality scans or unusual handwriting, accuracy drops to 80–85%. Production systems flag low-confidence extractions automatically for human review. This hybrid approach delivers practical accuracy rates above 99% on the final extracted data, combining machine speed with human accuracy on difficult cases.

Can LLMs make final coverage decisions on insurance claims?

LLMs assist coverage analysis. They should not make final binding coverage decisions on their own in current deployments. Regulatory requirements in most jurisdictions require human accountability for coverage determinations. LLMs generate coverage analysis and recommendations. Licensed adjusters make final determinations. This division of labor is both the regulatory-compliant and the highest-quality approach for automating insurance claims processing using OCR and LLMs today.

How long does it take to implement an automated claims system?

Implementation timelines depend heavily on scope and existing infrastructure. A focused pilot on one claim type with a modern core system integration takes three to six months. A full enterprise deployment across multiple claim lines with legacy system integration takes twelve to twenty-four months. Phased implementation starting with high-volume, low-complexity claims delivers ROI fastest while limiting early deployment risk.

What types of claims are easiest to automate first?

Simple, high-volume claim types deliver the fastest automation ROI. Pharmaceutical claims in health insurance are highly structured and respond well to full automation. Fender-bender auto claims with police reports and repair estimates are strong early targets. Simple life insurance claims with clear documentation requirements automate well. Complex liability claims, disputed injury claims, and large property losses require more sophisticated automation with strong human oversight.

Does automating claims processing eliminate adjuster jobs?

Early adopters report adjuster role transformation rather than elimination. Adjusters spend less time on data entry and more time on complex case analysis, fraud investigation, and policyholder communication. Overall adjuster headcount grows more slowly than claim volume. Some organizations redeploy adjusters to higher-value activities. Workforce planning for the transition requires deliberate management attention.

How does automation handle claims with missing documents?

The automation system identifies missing required documents during intake. It generates document request communications automatically. It tracks outstanding document requests and sends follow-up reminders. When documents arrive, it re-enters the processing queue immediately. This automated document management reduces the administrative burden on adjusters while improving completeness rates before adjudication begins.

Read More:-Transitioning from Manual QA to AI-Driven Automated Testing

Conclusion

Insurance claims processing carries a long history of inefficiency. The operational costs are significant. The human cost to claimants waiting weeks for resolution is real. Both are solvable problems with technology that exists today.

Automating insurance claims processing using OCR and LLMs delivers on the promise that AI made to the insurance industry years ago. OCR handles the document intake problem. LLMs handle the understanding problem. Together they compress cycle times, reduce costs, improve accuracy, and free adjusters to do the work that genuinely requires human judgment.

The technology is ready. The business case is proven. Early adopters demonstrate 40–60% cycle time reductions and 30–50% cost reductions on automated claim types. These numbers improve as models get better and teams learn to optimize their specific workflows.

The path forward is not full automation everywhere immediately. It starts with high-volume, well-defined claim types. It builds trust through transparency and measurable accuracy. It expands as the system proves itself. Insurers that start this journey now build the operational capability that becomes a durable competitive advantage as automating insurance claims processing using OCR and LLMs becomes the industry standard rather than the leading edge.

The claimant waiting for resolution deserves a faster answer. The adjuster buried in repetitive data entry deserves better work. The insurer carrying unsustainable processing costs deserves a smarter operation. This technology serves all three. Start building.